We all remember the spring of 2019 when historic water levels devastated local basements. Navigating the Muskoka river flooding impact on property insurance means recognizing that these unforeseeable weather events are a constant threat. According to the Insurance Bureau of Canada, water damage is now the number one cause of property claims provincially, driven heavily by our unique topography. So the big question remains, does home insurance cover water damage?

Most people mistakenly assume their standard policy covers every type of flood. Actually, typical home insurance for water damage in Muskoka, Ontario, usually applies the “Sudden and Accidental” rule—protecting you against a frozen pipe bursting without warning. Preparing for the rapid snowmelt, which creates severe spring freshet flood risks in bracebridge, requires recognizing that basic coverage often stops right at your exterior walls.

Securing true peace of mind demands specific “Endorsements,” which are simply optional coverage add-ons. Industry data reveals a critical legal distinction between surface water creeping across your lawn and municipal drains pushing waste backward into your home. Without the correct policy pieces for these distinct risks, you could easily be left footing a $40,000 repair bill alone.

The ‘Sudden and Accidental’ Rule: What Standard Home Insurance Actually Covers

When a deep February freeze hits Muskoka, you might ask, “will home insurance cover water damage if a pipe bursts?” The answer depends on the “Sudden and Accidental” rule. Insurers view standard coverage as a safety net for unpredictable emergencies, not a maintenance plan for aging plumbing. If a disaster happens instantly and you could not have prevented it, your basic policy is designed to step in.

It helps to know exactly what triggers this baseline protection. If you are wondering “does home insurance cover water damage?”, standard policies typically include these three sudden scenarios:

- A frozen pipe that bursts violently inside your wall

- A washing machine hose that snaps mid-cycle

- A water heater tank that ruptures without warning

Conversely, standard home insurance water damage exclusions almost always target gradual problems, like a slow sink drip that rots your floorboards over six months. Insurers classify these hidden, slow leaks as preventable maintenance, making them the leading reason for claim denials today. Yet, even if your home’s internal plumbing is perfectly maintained, community infrastructure can still fail. This makes specialized endorsements for sewer backup absolutely essential for local homeowners.

Sewer Backup Endorsements: Why This ‘Optional’ Coverage is a Must for Muskoka Homes

While a burst pipe is an internal issue, your home also faces plumbing threats from the streets. When Muskoka municipal storm drains get overwhelmed during heavy downpours, they create a “Reverse Flow” effect. Instead of water flowing away from your property, the sheer volume pushes municipal waste backward up through your basement floor drains.

Rural Muskoka property owners often assume their private septic tanks protect them from this specific municipal problem. However, heavy ground saturation can easily force your own septic waste back indoors during a severe storm. You might wonder, is sewer backup coverage mandatory in Ontario? It is strictly an optional endorsement, meaning you must specifically ask your broker to add it to your standard policy.

Weighing the small premium increase against the potential devastation makes adding this protection an easy choice. Reliable sewer backup coverage usually costs just a few extra dollars a month, but it pays for the mandatory biohazard cleanup and replacing ruined basement drywall.

Locating exactly where the water originated is crucial for making a successful claim. The main difference between sewer backup and overland water insurance relies on direction: did the mess push up through your plumbing, or did it flow across your lawn? That directional rule remains a critical distinction when assessing the various risks of the spring melt.

Overland Water vs. Groundwater: Mapping the Difference Before the Muskoka River Rises

Following that directional rule, watching the Muskoka River swell during the spring melt brings a familiar local anxiety. When water breaches those riverbanks and rushes across your lawn into a basement window, you face “Overland Water.” Securing proper overland flood insurance in the Muskoka region is critical because standard policies completely exclude this surface-level threat.

Conversely, water doesn’t always attack from above ground. As melting snow saturates our hilly terrain, it creates hydrostatic pressure—acting like a heavy, wet sponge squeezing against your concrete foundation. This pressure forces moisture upward through tiny, invisible basement floor cracks, highlighting the crucial difference of groundwater seepage vs surface water flooding.

| Threat Feature | Overland Water | Groundwater Seepage | | :— | :— | :— | | Origin Point | Overflowing rivers or rapidly pooling rain. | High subterranean water tables beneath the earth. | | Entry Method | Flowing through windows, doors, or vents. | Squeezing upward through foundation floor cracks. | | Coverage Trigger | Surface water breaching the home’s exterior. | Sub-surface pressure penetrating the concrete slab. | | Required Solution | Optional Overland Water Endorsement. | Optional Groundwater Endorsement. |

Evaluating your property’s specific topography dictates exactly which water damage coverage you actually need. If your home sits at the bottom of a steep Bracebridge driveway, you are highly vulnerable to both rapid surface runoff and intense, invisible underground pressure.

Mastering these definitions empowers you to verify your exact protections with your broker rather than guessing. Armed with this specific vocabulary, you are perfectly positioned to evaluate your true risk level and navigate local floodplain mapping effectively.

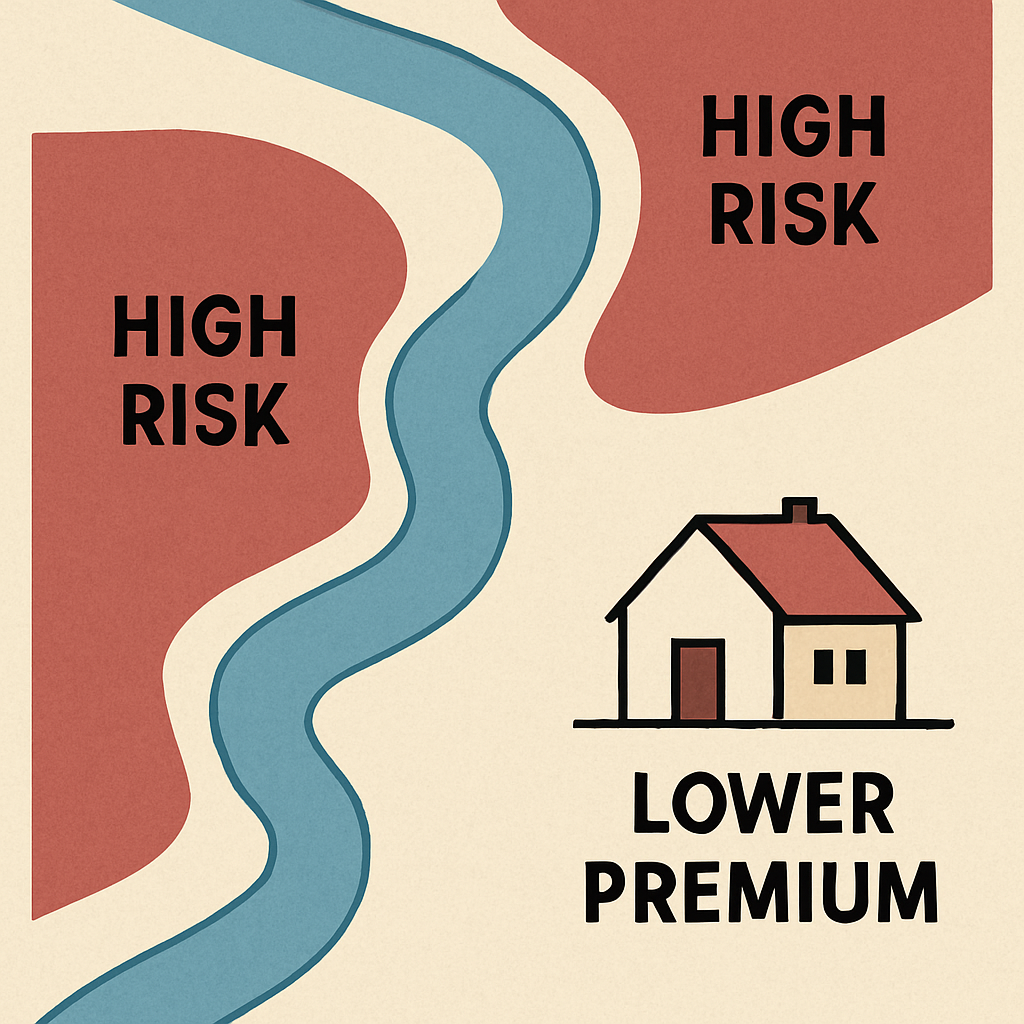

Surviving the Spring Freshet: Navigating Muskoka Floodplain Mapping and Insurance Rates

Every spring, the famous Muskoka freshet brings a rising water anxiety that directly impacts your wallet. Insurance companies rely heavily on municipal data to calculate your property’s specific risk level. Familiarity with Muskoka floodplain mapping and insurance rates provides a distinct advantage; if local charts place your lot inside a high-risk zone, your premiums will naturally reflect that danger.

A dangerous local myth is the assumption that the province will automatically bail you out after a severe storm. While the disaster recovery assistance for Ontarians program does exist, it only activates during formally declared emergencies and strictly covers bare essentials, ignoring finished basements entirely. Relying on this limited safety net instead of securing private flood insurance options through your broker is a highly costly gamble.

Checking your address against the District’s interactive flood maps lets you see exactly what the insurance companies see. Once you verify your geographic risk and confirm your endorsements, the final piece of the puzzle is physical defense. Implementing proactive steps to safeguard your property against these mapped threats is essential for keeping your home secure.

Preventing the Payout: Proactive Steps to Mitigate Residential Flood Damage

Knowing your flood zone is only half the battle; insurers expect you to defend your property before the Muskoka River crests. Taking proactive steps to mitigate residential flood damage does more than keep your basement dry—it often unlocks premium discounts and prevents claims from being denied due to homeowner negligence.

Prevention is worth thousands when navigating sump pump failure insurance coverage, which generally demands proof of routine upkeep before paying out. To satisfy your insurer’s strict mitigation requirements, implement this mandatory seasonal checklist:

- Install a backwater valve to stop full municipal pipes from reversing into your drains.

- Test your sump pump battery backup before the heavy spring melt.

- Direct exterior downspouts at least six feet away from your foundation.

- Ensure your lot grading forces surface water away from the house.

- Seal visible foundation cracks before the ground completely thaws.

Beyond your walls, older Muskoka properties face a completely different hidden threat. If the main underground pipe connecting your home to the town’s water supply collapses or freezes, standard water policies won’t help. Adding specific service line coverage for water pipe repairs is vital, as you are financially responsible for this exterior plumbing right up to your property line.

Even with pristine maintenance and proactive upgrades, nature occasionally overwhelms our local infrastructure. When water starts rising in the dark, your immediate actions will directly dictate your financial recovery and claim success.

The 2:00 AM Disaster Plan: How to File a Water Damage Claim and Get Paid

It’s 2:00 AM, a severe Muskoka storm kills the power, and water is sloshing across your basement floor. Before calling your broker, you must fulfill the “Duty to Mitigate”—which simply means taking immediate action to stop the bleeding. Whether defending your Muskoka home or handling seasonal cottage water damage prevention, insurers expect you to move valuables upstairs and call a plumber. Simply watching the water rise invites a claim denial for negligence.

After containing the immediate threat, you must legally demonstrate what was destroyed through a “Proof of Loss” document. Mastering how to file a water damage insurance claim successfully relies entirely on the evidence you gather before cleanup finishes. Build your official claim using this essential documentation kit:

- Time-stamped photos and videos of the standing water.

- Original receipts verifying the value of ruined electronics or furniture.

- A written room-by-room inventory list noting the age of damaged goods.

- Invoices and contractor contacts for any emergency temporary repairs.

Hiring a local restoration company immediately ensures professional drying, preventing hazardous mold before an adjuster even arrives. Acting swiftly maximizes your comprehensive water damage endorsement benefits, guaranteeing fair and prompt payouts. To ensure your policy actually covers these messy midnight disasters, conducting a quick insurance audit with your broker is the best proactive measure.

Your 5-Minute Insurance Audit: Four Questions to Ask Your Broker Today on Insurance Coverage for Water Damage

You no longer have to cross your fingers when the spring snow melts along the Muskoka River. With a clear picture of home insurance for water damage in Muskoka, Ontario, you can now spot coverage gaps before a basement drain starts gurgling. Finding those missing pieces—whether it’s an Overland Water or a Sewer Backup endorsement—replaces seasonal anxiety with genuine peace of mind.

Grab your paperwork for a five-minute review, then confidently call your provider to secure a localized strategy. Ask them these three specific questions:

- Do I have the specific endorsement for Overland Water?

- Is my water damage coverage limit high enough to replace a fully finished basement?

- Does my policy protect against groundwater seepage?

- Does my home insurance cover water damage and what are the clauses?

Need a Professional Roofing and Exteriors Company to Help With Repairs?

If your property has been hit by the recent floods and you’re unsure what to do or where to start, give us a call and we’ll guide you through this rough time. We know it can be daunting at best and that’s why it’s helpful to have a professional in your corner to offer sound advice and help with any potential repairs. For a completely free and no-obligation assessment, get in touch and we’ll send our Assessment Specialist out to your property. Stay safe and we got your back!